TAcharts 0.0.29

By: Carl Farterson

Contributors: @rnarciso, @t3ch9

This repository provides technical tools to analyze OHLCV data, along with several TA chart functionalities. These functions are optimized for speed and utilize numpy vectorization over built-in pandas methods when possible.

Methods

Indicators With Chart Functionality

-

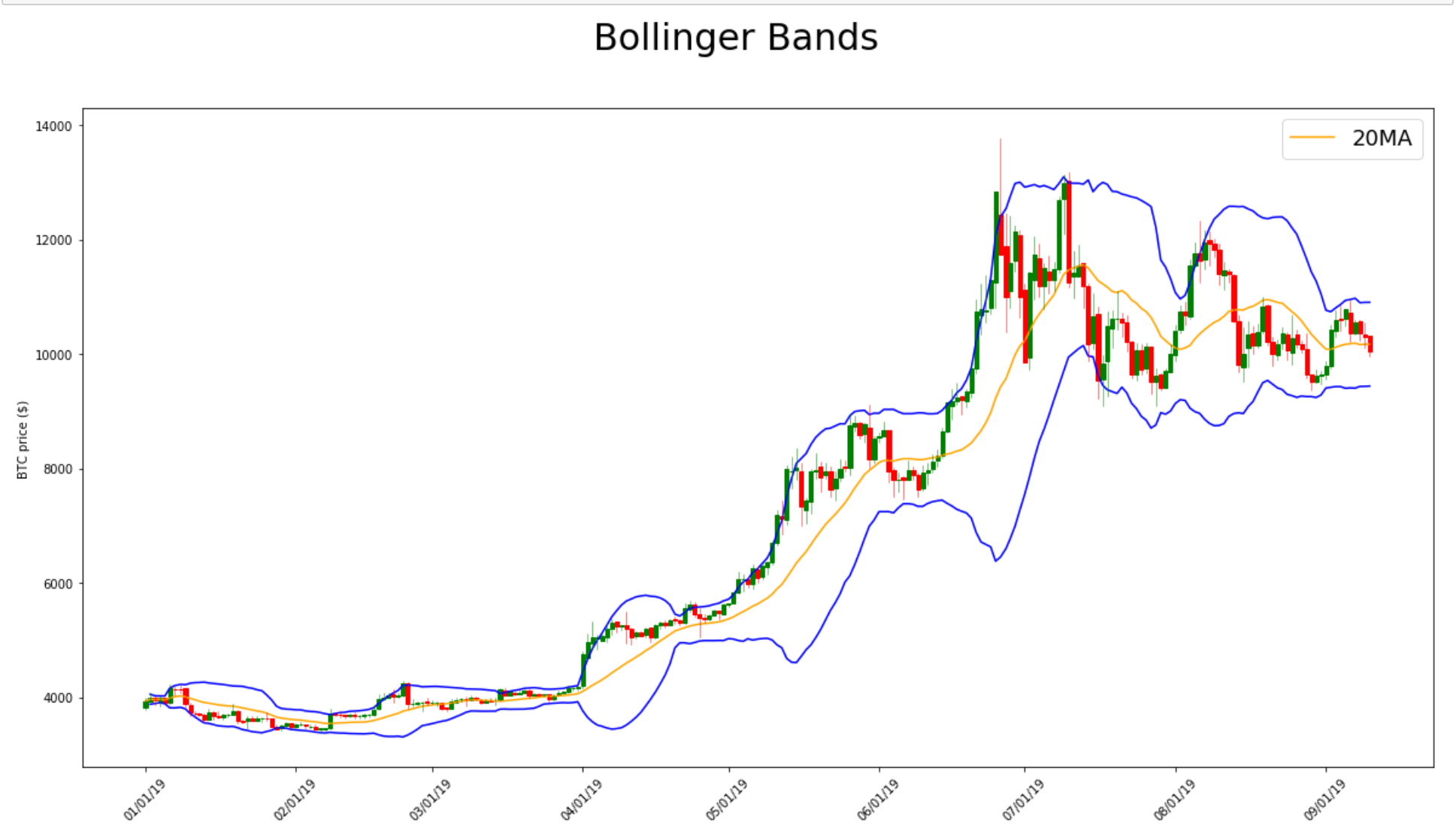

Bollinger(df=None, filename=None, interval=None, n=20, ndev=2): Bollinger Bands -

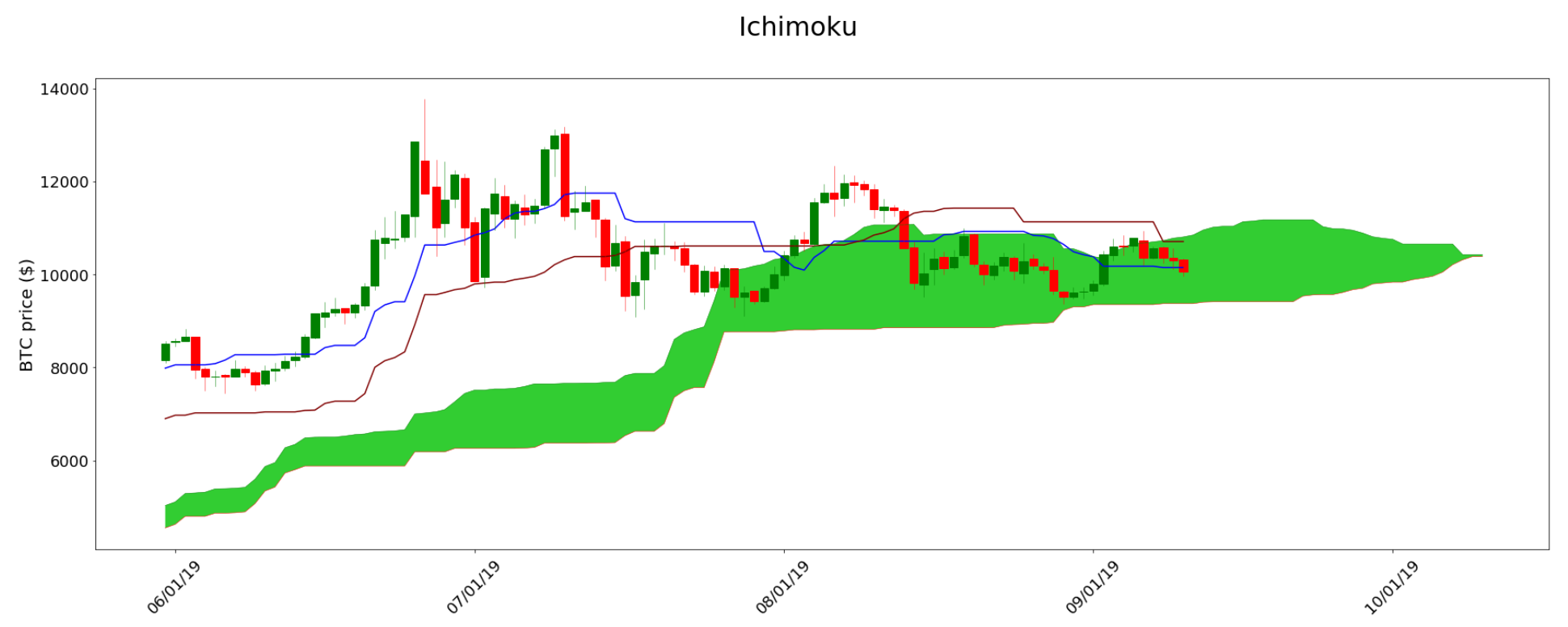

Ichimoku(df=None, filename=None, interval=None): Ichimoku Cloud -

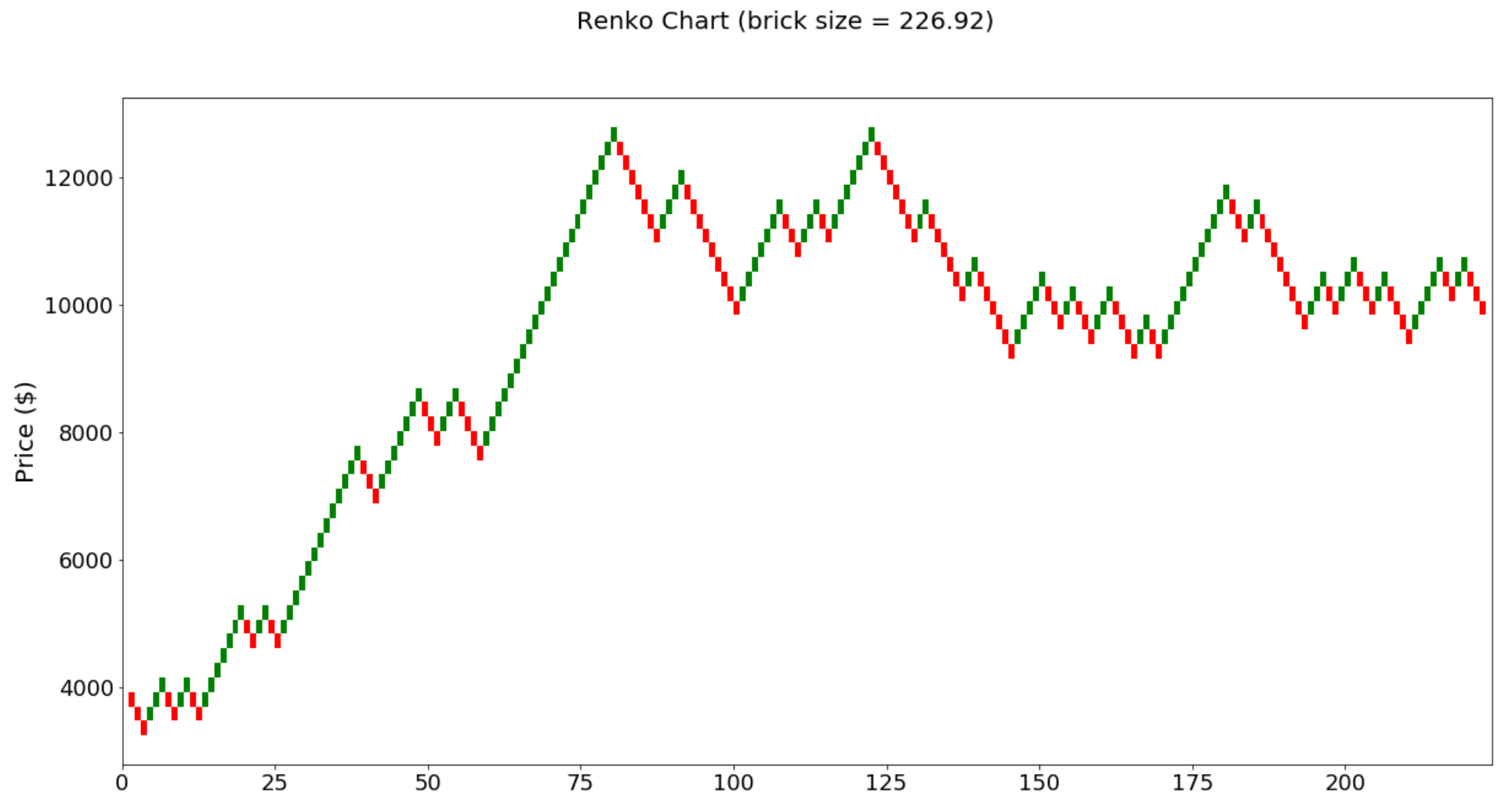

Renko(df=None, filename=None, interval=None): Renko Chart

Indicators Without Chart Functionality

-

atr(high, low, close, n=2): average true range from candlestick data -

cmf(df, n=2): Chaikin Money Flow of an OHLCV dataset -

double_smooth(src, n_slow, n_fast): The smoothed value of two EMAs -

ema(src, n=2): exponential moving average for a list ofsrcacrossnperiods -

macd(src, slow=25, fast=13): moving average convergence/divergence ofsrc -

mmo(src, n=2): Murrey Math oscillator ofsrc -

roc(src, n=2): rate of change ofsrcacrossnperiods -

rolling(src, n=2, fn=None, axis=1): rollingsum,max,min,mean, ormedianofsrcacrossnperiods -

rsi(src, n=2): relative strength index ofsrcacrossnperiods -

sdev(src, n=2): standard deviation across n periods -

sma(src, n=2): simple moving average ofsrcacrossnperiods -

td_sequential(src, n=2): TD sequential ofsrcacrossnperiods -

tsi(src, slow=25, fast=13): true strength indicator

utils

-

area_between(line1, line2): find the area between line1 and line2 -

crossover(x1, x2): find all instances of intersections between two lines -

draw_candlesticks(ax, df): add candlestick visuals to a matplotlib chart -

fill_values(averages, interval, target_len): Fill missing values with evenly spaced samples.- Example: You're using 15-min candlestick data to find the 1-hour moving average and want a value at every 15-min mark, and not every 1-hour mark.

-

group_candles(df, interval=4): combine candles so instead of needing a different dataset for each time interval, you can form time intervals using more precise data.- Example: you have 15-min candlestick data but want to test a strategy based

on 1-hour candlestick data (

interval=4).

- Example: you have 15-min candlestick data but want to test a strategy based

on 1-hour candlestick data (

-

intersection(a0, a1, b0, b1): find the intersection coordinates between vector A and vector B

How it works

Create your DataFrame

# NOTE: we are using 1-hour BTC OHLCV data from 2019.01.01 00:00:00 to 2019.12.31 23:00:00

from TAcharts.utils.ohlcv import OHLCV

df = OHLCV().btc

df.head()| date | open | high | low | close | volume | |

|---|---|---|---|---|---|---|

| 0 | 2019-01-01 00:00:00 | 3699.95 | 3713.93 | 3697.00 | 3703.56 | 660.279771 |

| 1 | 2019-01-01 01:00:00 | 3703.63 | 3726.64 | 3703.34 | 3713.83 | 823.625491 |

| 2 | 2019-01-01 02:00:00 | 3714.19 | 3731.19 | 3707.00 | 3716.70 | 887.101362 |

| 3 | 2019-01-01 03:00:00 | 3716.98 | 3732.00 | 3696.14 | 3699.95 | 955.879034 |

| 4 | 2019-01-01 04:00:00 | 3699.96 | 3717.11 | 3698.00 | 3713.07 | 534.113945 |

Bollinger Bands

from TAcharts.indicators.bollinger import Bollinger

b = Bollinger(df)

b.build(n=20, ndev=2)

b.plot()

Ichimoku

from TAcharts.indicators.ichimoku import Ichimoku

i = Ichimoku(df)

i.build(20, 60, 120, 30)

i.plot()

Renko

from TAcharts.indicators.renko import Renko

r = Renko(df)

r.set_brick_size(auto=True, atr_interval=2)

r.build()

r.plot()

wrappers

-

@args_to_dtype(dtype): Convert all function arguments to a specific data typefrom TAcharts.wrappers import args_to_dtype # Example: `src` is converted to a list @args_to_dtype(list) def rsi(src, n=2): pass

-

@pd_series_to_np_array: Convert function arguments frompd.Seriestonp.arrayusingpd.Series.values. This wrapper is 10x quicker than using@args_to_dtype(np.array)when working with Pandas series.from TAcharts.wrappers import pd_series_to_np_array # Example: `high`, `low`, and `close` are all converted into `np.array` data types @pd_series_to_np_array def atr(high, low, close, n=14): pass